Overview of DPR Inventory, Storage, and Ownership Classifications

| Published: Jan 22, 2026 | Accounting , Grain , Tips | read

read

readThis document outlines the key inventory, storage, and company‑owned categories used within the Daily Position Report (DPR). Each classification represents a specific stage or status of commodities as they move through procurement, storage, and sales processes.

Understanding these categories ensures consistent reporting, accurate valuation, and improved operational visibility across facilities.

Inventory

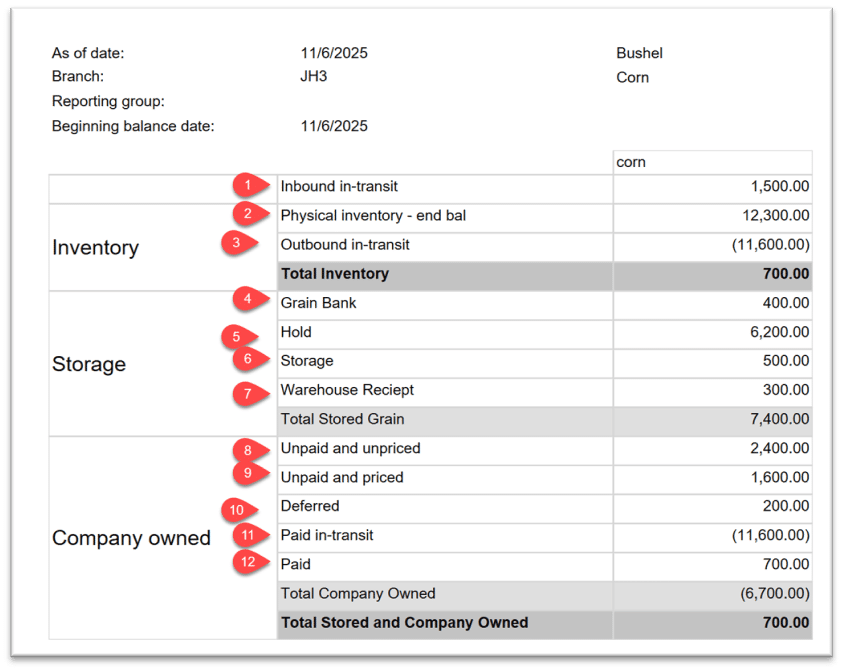

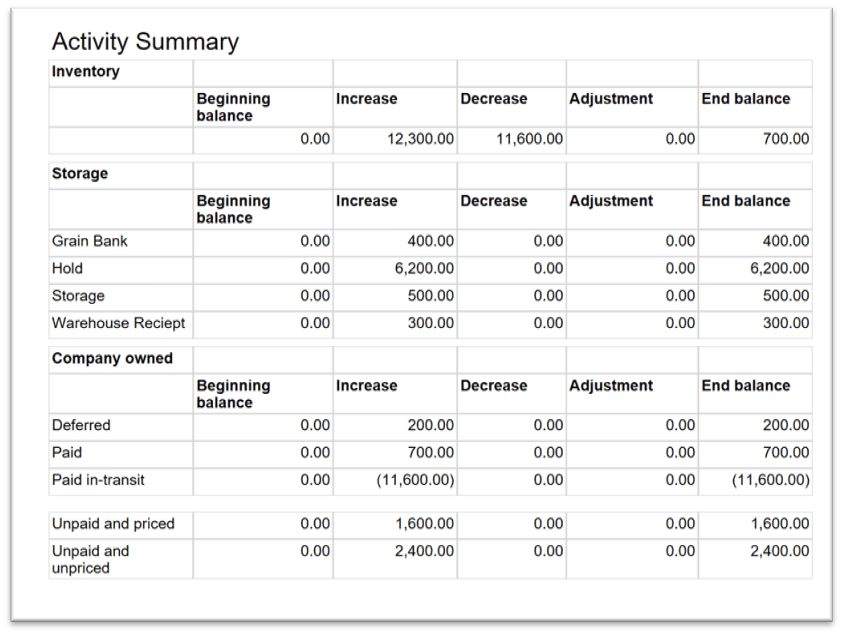

1. Inventory: Inbound in-transit – These are inbound in-transit tickets that are entered into the system. Does not matter if they are applied to contracts or not. This is a record of commodities that have shipped from the vendor and are on the way to the facility. This total is the sum of the origin weights of these tickets. When received at the facility they will get an inbound ticket with the destination weights and grades matched to this in-transit ticket.

2. Inventory: Physical inventory – This is the quantity in inventory on-hand at that site plus any inbound tickets that are not posted yet. Including unapplied tickets in the DPR is an option in DPR parameters. Depending on that setting, the report might not include unposted tickets.

3. Inventory: Outbound in-transit – These are outbound tickets entered in the system. It does not matter if these are applied to contracts or not. If they are applied to contracts the qty that is displayed is based on the governing weights and grades of the applied contract (origin or destination). When an outbound ticket is invoiced, it is taken out of outbound in-transit.

Storage

4. Storage: Grain Bank – This is a total of the inbound tickets that are applied to storage agreements with the disposition of Grain bank. The company does not technically own this inventory. It is at their facility on behalf of the grower and is intended to be used by the facility to produce feed for the grower and will be returned to the grower as a part of another product.

5. Storage: Hold – This number represents inbound tickets that are not applied to a purchase contract or storage agreement. If the DPR parameter is set to include unposted tickets, this total will also include those unposted tickets.

6. Storage: Storage –These are inbound tickets that are applied to storage agreements with the disposition of storage. In this case, the grower has not committed to selling the commodity to the company, so the company is holding it for them until they decide. If the facility does not purchase the stored commodity, the commodity will go back to the grower.

7. Storage: Warehouse receipts – These are tickets that are on storage agreements, but have an issued warehouse receipt. Until the warehouse receipt is canceled, the company cannot purchase this quantity because it is being used as collateral by the grower. A warehouse receipt for a commodity is a document that serves as proof of ownership of goods, such as agricultural products or precious metals, stored in a warehouse. This receipt can be used to transfer ownership without physically moving the commodity, or it can be used as collateral to secure financing. It includes details like the type and quantity of goods, their location, and the date of issuance.

Company Owned

8. Company owned: Unpaid and unpriced – These are inbound tickets applied to purchase contracts that are either unpriced, board only, or basis only. They are not fully priced

9. Company owned: Unpaid and priced – These are inbound tickets applied to fully priced purchase contracts.

10. Company owned: Deferred – These are inbound tickets that have been invoiced (settled) but are not scheduled to be paid until a later date. The grower has agreed to be paid at a price. And the company now owns the commodity, but the grower has agreed to be paid at a future date. Generally, this is due to tax purposes for the grower. The grower wants to defer getting paid for the commodity to lower their income for the year for tax reporting purposes. They have agreed to get paid the next calendar year.

11. Company owned: Paid in-transit – This is a total of the outbound scale tickets. This should match the Outbound in-transit in the inventory section.

12. Company owned: Paid – This is a total of the inbound tickets that have been paid (settlement has payment against it) and outbound tickets have been delivered through sales orders.

For more information, visit our YouTube channel and Commodity Accounting section.